THE HSA MILLIONAIRE: How to Build $1 Million in Tax-Free Wealth Using a Health Savings Account

How to Build $1 Million in Tax-Free Wealth Using a Health Savings Account

Most people think of Health Savings Accounts (HSAs) as a way to save a few hundred dollars on medical expenses. But what if I told you that your HSA could be the most powerful

wealth-building tool you're not capable of growing to over $1 million in tax-free money?

After 7+ years as an employee benefits consultant, I've seen thousands of people leave money on the table by treating their HSA like a checking account instead of the retirement superpower it actually is.

Let me show you the strategy that financial planners don't talk about enough and why the HSA might be even better than your 401(k).

THE TRIPLE TAX ADVANTAGE: BETTER THAN A 401(K) OR ROTH IRA

Here's what makes the HSA truly unique it's the ONLY account in the U.S. tax code with a triple tax advantage:

TAX DEDUCTION ON CONTRIBUTIONS (like a 401(k))

Every dollar you contribute reduces your taxable income. If you're in the 24% tax bracket and contribute $8,300 (2026 family limit), you save nearly $2,000 in taxes immediately.

TAX-FREE GROWTH (like a Roth IRA)

Your HSA investments grow completely tax-free. No capital gains taxes. No dividend taxes. Ever.

TAX-FREE WITHDRAWALS (better than everything else)

When you use the money for qualified medical expenses, you pay ZERO taxes. Not now. Not in retirement. Never.

Compare this to a 401(k) (taxed on withdrawal) or a Roth IRA (no upfront deduction). The HSA gives you the best of both worlds PLUS more.

THE MATH: HOW YOU GET TO $1 MILLION

Let's run the numbers. This isn't theoretical, it's based on actual contribution limits and historical market returns.

SCENARIO 1: THE CONSISTENT SAVER (Ages 30-65)

Starting age: 30

Retirement age: 65 Time horizon: 35 years

Annual contribution: $8,750 (2026 family HSA limit) Annual return: 8% (historical stock market average) Total contributions over 35 years: $306,250

Final HSA balance at age 65: $1,507,734.38

Yes, you read that right: $1.37 MILLION. Tax-free.

SCENARIO 2: THE LATE STARTER assume you are a family (Ages 45-65) Starting age: 45

Retirement age: 65 Time horizon: 20 years

Annual contribution: $8,750.00 Annual return: 8%

Total contributions: $175,000 Final balance: $400,421.88

Even starting at 45, you can build over $400K in tax-free wealth.

SCENARIO 3: THE CATCH-UP CHAMPION assume you are a family (Ages 55-65) Starting age: 55

Catch-up contribution: $8,750 ($1,000 extra for 55+) Time horizon: 10 years

Annual return: 8%

Total contributions: $97,000 Final balance: $141,241

Starting late? You can still build serious wealth.

THE STRATEGY: STOP SPENDING, START INVESTING

Here's where most people get it wrong: they treat their HSA like a debit card, spending every dollar on doctor visits and prescriptions.

Instead, the millionaire strategy is this:

✅ MAX OUT your HSA contributions every year

✅ INVEST the money in low-cost index funds (don't leave it in cash!)

✅ PAY medical expenses out-of-pocket from your checking account

✅ SAVE all your medical receipts (no expiration date!)

✅ LET the HSA grow tax-free for decades

✅ REIMBURSE yourself in retirement (tax-free!) using those old receipts

That's right you can pay medical expenses today, save the receipts, and reimburse yourself 20-30 years later, tax-free. The IRS has no time limit on reimbursements.

This turns your HSA into a stealth retirement account that never gets taxed.

THE REAL-WORLD EXAMPLE

Let me show you how powerful this is with a real scenario:

Meet Sarah, age 35, married with two kids:

⦁ 2026 HSA contribution: $8,750

⦁ Tax bracket: 24% federal + 6% state = 30% total

⦁ Immediate tax savings: $2,625

Sarah invests her HSA in a target-date index fund. She pays her $3,000 in annual medical expenses out of her checking account and saves all receipts in a folder.

Over 30 years:

⦁ Total HSA contributions: $272,500

⦁ Tax savings from contributions: 102,596

⦁ HSA growth at 8%: $1,086.171

⦁ Medical receipts accumulated: $90,000 (reimbursable tax-free anytime)

At age 65, Sarah has:

✅ $1,086,000 in tax-free HSA money

✅ $90,000 she can withdraw immediately (using old receipts)

✅ Saved $74,700 in taxes along the way

Total benefit: Over $1.1 million, completely tax-free.

Compare that to if Sarah had put the same money in a 401(k):

⦁ She'd owe taxes on every withdrawal (24%+ in retirement)

⦁ That $1M becomes $760K after taxes

⦁ She loses $240,000 to the IRS

The HSA saved her a quarter million dollars in taxes.

THE 5-STEP MILLIONAIRE HSA STRATEGY

Here's your actionable playbook:

STEP 1: ENROLL IN AN HSA-ELIGIBLE HIGH-DEDUCTIBLE HEALTH PLAN (HDHP)

Check with your employer or shop the marketplace for an HDHP. For 2026, the plan must have:

⦁ Minimum deductible: $1,650 individual / $3,300 family

⦁ Maximum out-of-pocket: $8,050 individual / $16,100 family

STEP 2: MAX OUT YOUR CONTRIBUTIONS

2026 contribution limits:

⦁ Individual: $4,150

⦁ Family: $8,750

⦁ Age 55+ catch-up: Extra $1,000

Set up automatic contributions from your paycheck (pre-tax) or contribute directly and deduct it on your tax return.

STEP 3: INVEST YOUR HSA (DON'T LEAVE IT IN CASH!)

This is the most important step most people miss. Your HSA provider should offer investment options, usually index funds or target-date funds.

Keep $1,000-2,000 in cash for emergencies, invest the rest. Recommended allocation:

⦁ Under 40: 90% stocks, 10% bonds

⦁ 40-55: 70% stocks, 30% bonds

⦁ 55-65: 60% stocks, 40% bonds

⦁ After 65: You can use it for anything (with income tax if not medical)

STEP 4: PAY MEDICAL EXPENSES OUT-OF-POCKET & SAVE RECEIPTS

Pay your doctor bills, prescriptions, dental, and vision expenses from your regular checking account NOT your HSA.

Save every receipt. Create a folder (digital or physical) organized by year.

Qualified expenses include:

✅ Doctor visits and hospital care

✅ Prescriptions

✅ Dental and vision care

✅ Mental health services

✅ Chiropractors and acupuncture

✅ Medical equipment

✅ Over-the-counter medications (with prescription)

✅ Medicare premiums (after age 65)

STEP 5: LET IT GROW FOR DECADES

Don't touch it. Let compound growth do the heavy lifting. At 8% annual returns:

⦁ After 10 years: $120,000

⦁ After 20 years: $411,000

⦁ After 30 years: $1,024,000

⦁ After 35 years: $1,376,000

AFTER AGE 65: YOUR HSA BECOMES EVEN MORE FLEXIBLE

Here's the beautiful part at age 65, your HSA becomes incredibly flexible:

✅ OPTION 1: Withdraw for medical expenses (tax-free forever)

Use it for Medicare premiums, prescriptions, long-term care, dental, vision all tax-free.

✅ OPTION 2: Reimburse yourself for old medical expenses (tax-free) Remember those 30+ years of receipts? Cash them in, tax-free.

✅ OPTION 3: Use it for anything (taxed like a Traditional IRA)

After 65, you can withdraw for non-medical expenses and just pay income tax (no 20% penalty). It essentially becomes a Traditional IRA.

So in the worst case, it's as good as your 401(k). Best case, it's completely tax-free. COMMON MISTAKES THAT COST YOU MONEY

After working with hundreds of clients on their HSAs, here are the biggest mistakes I see:

❌ MISTAKE 1: Not enrolling in an HSA at all

33% of eligible employees don't open an HSA. They're leaving thousands in tax savings on the table.

❌ MISTAKE 2: Contributing but not investing

The average HSA balance is $4,300, and 90% of it sits in cash earning 0.1%. That's like parking a Ferrari in the garage and never driving it.

❌ MISTAKE 3: Spending HSA money on small medical bills

That $50 prescription costs you $500+ in future growth if you pay from your HSA instead of out-of-pocket.

❌ MISTAKE 4: Not saving receipts

Without receipts, you lose the ability to reimburse yourself tax-free later.

❌ MISTAKE 5: Thinking "I'm healthy, I don't need an HSA"

That's exactly WHY you need it! Healthy = fewer expenses = more money stays invested = millionaire status.

❌ MISTAKE 6: Forgetting the catch-up contribution at 55

That extra $1,000/year for 10 years = $15,000+ in additional wealth.

❌ MISTAKE 7: Withdrawing for non-medical expenses before 65 20% penalty PLUS income tax. Ouch. Don't do it.

WHO IS THIS STRATEGY FOR?

The HSA millionaire strategy works best if you:

✅ Are relatively healthy and don't have chronic conditions requiring frequent care

✅ Can afford to pay medical expenses out-of-pocket

✅ Have 20+ years until retirement

✅ Are maximizing other retirement accounts (401k, IRA)

✅ Want to minimize lifetime taxes

✅ Are disciplined about not touching the money

Who should be cautious:

⚠ People with chronic conditions requiring expensive ongoing treatment

⚠ Families who can't afford to pay medical bills out-of-pocket

⚠ Those living paycheck-to-paycheck

⚠ People who need the tax deduction from large medical expenses

For most healthy individuals and families, though, this is a game-changer. THE EMPLOYER MATCH: FREE MONEY

Here's a bonus many people don't know about: some employers contribute to your HSA!

Common employer HSA contributions:

⦁ $500-1,000 for individuals

⦁ $1,000-2,000 for families

This is FREE money. Always contribute at least enough to get the full employer match.

Example: If your employer contributes $1,500 to your family HSA and you contribute the remaining $6,800 to max it out, you're really only paying $6,800 but getting $8,300 of value. Over 35 years, that employer contribution alone grows to $247,000 tax-free.

Adding State Taxes

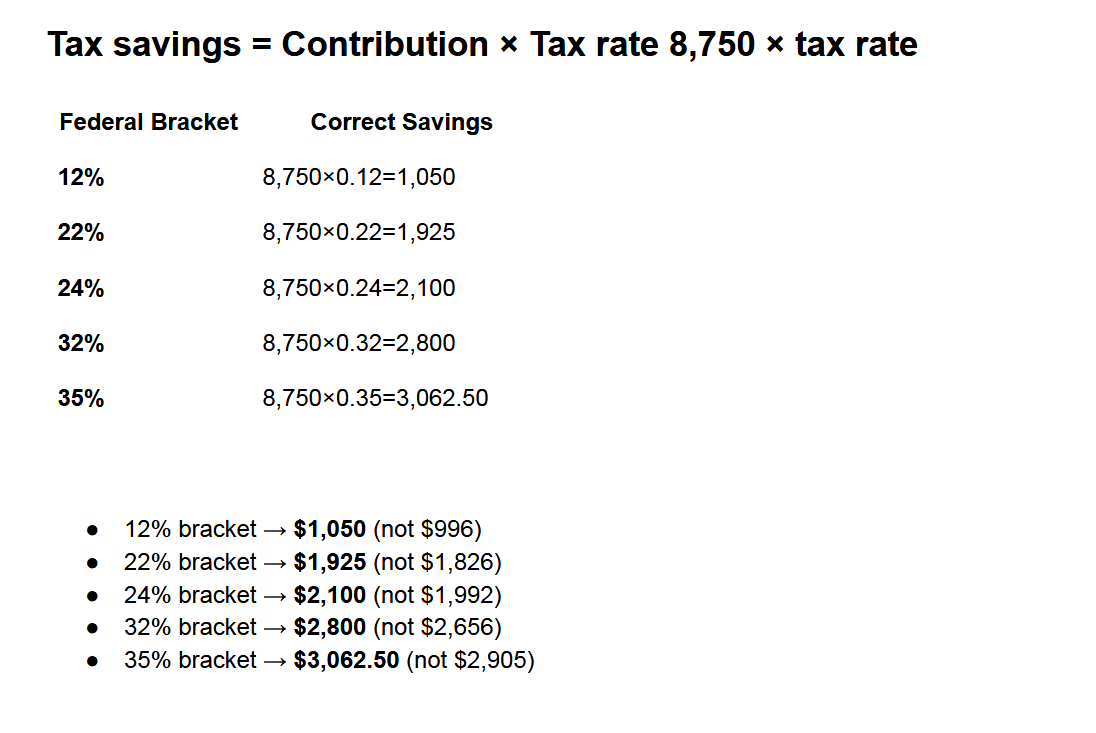

If your state tax is 3–8%, then:

8,750×0.03=262.50

8,750×0.08=700

So total tax savings (federal + state) becomes:

⦁ Low end: 1,050+262.50=1,312.50

⦁ High end: 3,062.50+700=3,762.50

$1,313 – $3,763 per year

35-Year Tax Savings

Annual savings:

Low end:

1,313×35=45,955

High end:

3,763×35=131,705

$46,000 – $132,000 in tax savings before investment growth.

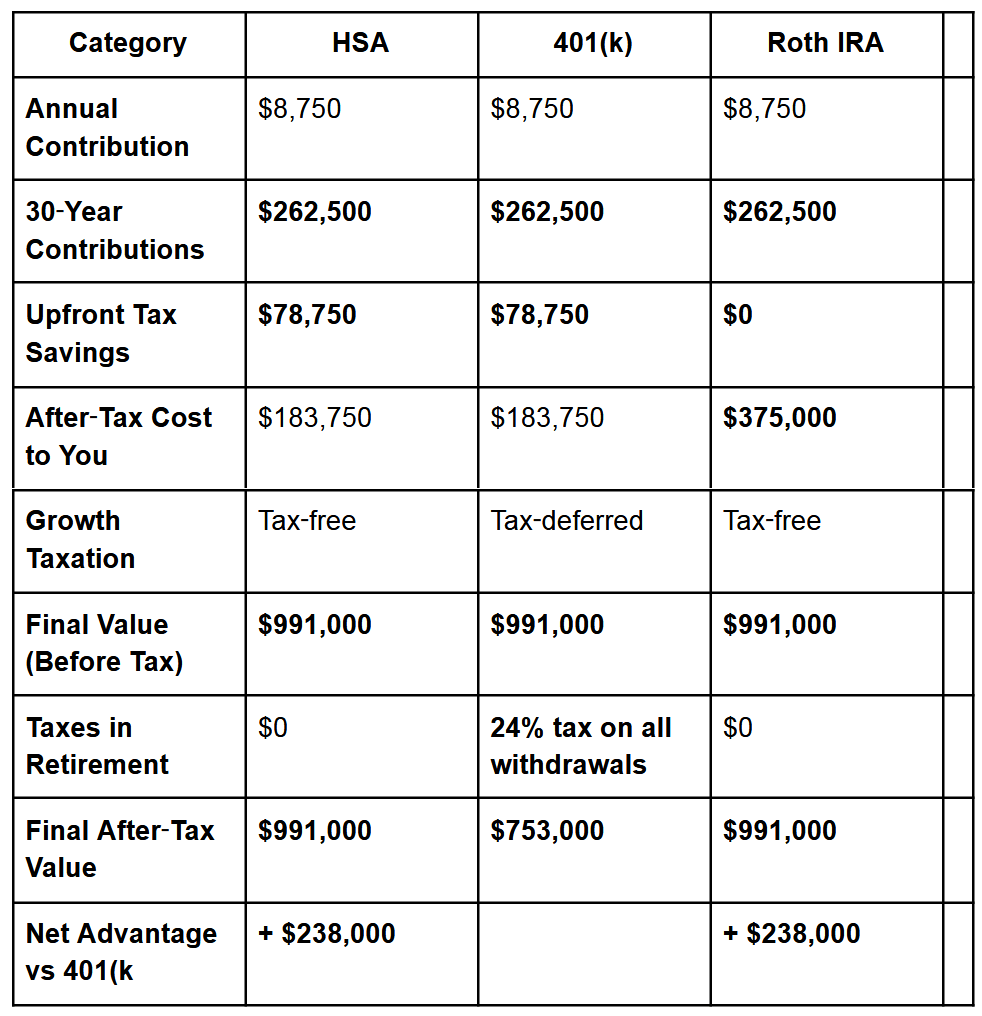

Let's settle this once and for all. If you invest $8,750/year for 30 years at 8% returns:

HSA:

⦁ Contributions: $262,500 (pre-tax)

⦁ Tax savings upfront: 78,750 (at 30% bracket)

⦁ Growth: Tax-free

⦁ Withdrawals: Tax-free (medical)

⦁ Final value: 991,200 (completely tax-free)

401(K):

⦁ Contributions: $262,500 (pre-tax)

⦁ Tax savings upfront: $78,750

⦁ Growth: Tax-deferred

⦁ Withdrawals: Fully taxable at 24%

⦁ Final value:$991,000 →$753,000 after taxes

ROTH IRA:

⦁ Contributions: $262,500 (after-tax, so actually costs you $375,000 to contribute)

⦁ Tax savings upfront: $0

⦁ Growth: Tax-free

⦁ Withdrawals: Tax-free

⦁ Final value:$991,000 (tax-free)

📊 HSA vs 401(k) vs Roth IRA

Assumptions:

⦁ $8,750/year contribution

⦁ 30 years

⦁ 8% annual return

⦁ 30% tax bracket (for upfront tax effects)

⦁ 401(k withdrawal tax: 24%

🟩 Final Comparison Table

🧠Key Takeaways

🟩 HSA is the most powerful account in the U.S. tax code

⦁ Triple tax advantage:

Tax‑free in → Tax‑free growth → Tax‑free out

⦁ Beats both 401(k) and Roth IRA in total tax savings and after‑tax value.

🟦 Roth IRA is second best

⦁ Same final value as HSA

⦁ But costs twice as much to fund because contributions are after‑tax.

🟧 401(k) is still great but the least efficient of the three

⦁ You save taxes upfront

⦁ But you lose a big chunk in retirement

⦁ Ends up $238,000 behind the HSA and Roth IRA over 30 years

🔥 Bottom Line

If your goal is maximum long‑term wealth, the ranking is:

- HSA (best overall)

- Roth IRA

- 401(k)

- Winner: HSA (if used for medical expenses)

- Runner-up: Roth IRA (but you have to pay taxes upfront)

- Third place: 401(k) (you pay taxes on the back end)

The HSA gives you the best of both worlds.

REAL TALK: CAN YOU REALLY BECOME A MILLIONAIRE?

Yes but you need three things:

TIME: Start early (ideally in your 30s) or commit to aggressive catch-up contributions CONSISTENCY: Max it out every single year without fail

DISCIPLINE: Don't touch the money. Pay medical expenses out-of-pocket.

Is it easy? No.

Is it worth it? Absolutely.

$1 million in tax-free money that you can use for medical expenses (which we all have more of as we age) is an incredible retirement asset.

And even if you don't hit $1M, getting to $400K, $600K, or $800K is still life-changing.

ACTION STEPS: START YOUR HSA MILLIONAIRE JOURNEY TODAY

Ready to start building tax-free wealth? Here's what to do:

☑ STEP 1: Check if you're eligible for an HSA

Ask your HR department if your health plan is HSA-eligible (HDHP). If not, consider switching during open enrollment.

☑ STEP 2: Open your HSA

Your employer may have a designated HSA provider. If not, consider Fidelity, Lively, or HealthEquity (low fees, good investment options).

☑ STEP 3: Set up automatic maximum contributions Individual: $4,150 (2026)

Family: $8,300 (2026) Age 55+: Add $1,000

☑ STEP 4: Invest your HSA (don't leave it in cash!)

Choose a low-cost index fund or target-date fund. Set it and forget it.

☑ STEP 5: Create a receipt filing system

Digital folder or physical accordion folder—organized by year. Save EVERYTHING.

☑ STEP 6: Pay medical expenses out-of-pocket Use your checking account, not your HSA card.

☑ STEP 7: Review and adjust annually

Check your HSA balance, rebalance investments, and celebrate your progress. FINAL THOUGHTS: THE HSA IS HIDING IN PLAIN SIGHT

I've been a benefits consultant for over 7 years, and I'm constantly amazed by how many people overlook the HSA.

It's not flashy. It's not exciting. It doesn't have the same name recognition as a 401(k) or IRA. But it might be the single best tax-advantaged wealth-building tool available to Americans today.

If you're healthy, disciplined, and thinking long-term, the HSA millionaire strategy could change your retirement.

The question isn't "Can you become a millionaire with an HSA?" The question is: "Why aren't you starting today?

INDIVIDUAL HSA ENROLLMENT

For Employer & Employee Enrollment

Book a time on my calendar: Book A TIME 45 MIN

YOUR TURN

Are you maximizing your HSA? What's holding you back?

And if this was helpful, please share it with someone who could benefit from the HSA millionaire strategy. Let's help more people build tax-free wealth.

Connect With Us

Explore our innovative solutions tailored just for you. Our team is ready to assist with your inquiries and provide exceptional support. Reach out to start your journey with us today.

Contact Me

Give us a call

(917) 780-6519Send us an email

[email protected]